401k_reform

Can You Convert Your 401(k) into a "Guaranteed Lifetime Monthly Income" While Still Working? A 2026 Development Worth Watching

Many people share a common anxiety about retirement savings: having money in the account, but not knowing how to draw it down without outliving their assets.

Congress is now pushing forward a reform aimed at answering this question—allowing you to lock in a portion of your 401(k) as a fixed monthly "lifetime income" stream before you even retire.

What Are the Current Rules?

Under current rules, you generally must separate from service or reach age 59½ before you can move your 401(k) funds elsewhere. Until then, the money is essentially locked inside the plan—your only options are choosing among the available investment options and watching your balance fluctuate with the market.

For those approaching retirement, this window is actually the most stressful period—if the market drops sharply one or two years before you retire, decades of accumulated savings could take a significant hit.

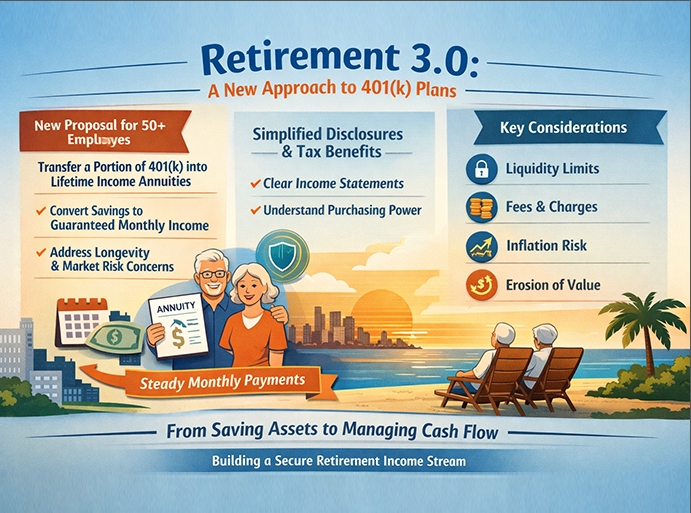

What Does the New Proposal Change?

A bipartisan bill jointly introduced by Democratic Representative Jimmy Panetta and Republican Representative Darin LaHood is pushing for one key change:

Allowing employees aged 50 and older to roll over a portion of their 401(k) assets into a qualifying annuity (Annuity) product while still employed—without needing to separate from service.

Simply put: you don't have to wait until retirement—you can convert a portion of your savings early into a fixed income that arrives in your account every month going forward. That money is no longer subject to market swings. Whether you live to 80 or 95, you'll receive a payment every month.

This directly addresses a very real risk—outliving your money.

How Does This Relate to SECURE 2.0?

This proposal is a significant extension of the SECURE 2.0 Act, passed in 2022.

SECURE 2.0 already encouraged employers to incorporate annuity options into their 401(k) benefit packages, but many companies have been holding back—primarily over one concern: if something goes wrong with the annuity provider, would the employer be held liable? The new bill further clarifies the scope of employer safe harbor protections, reducing the legal barriers to offering annuity options.

Additionally, the bill requires the IRS to rewrite the Section 402(f) rollover notice—currently a document filled with legal jargon that most people can't understand. The new version would require plain-language disclosures telling employees exactly how their taxes will be calculated after a rollover, how they can access their funds, and how much they can expect to receive each month.

Why Does 2026 Matter Particularly for This?

The lessons from market volatility are still fresh:

Over the past two years, elevated interest rates and stock market turbulence have reminded many near-retirees that being fully invested in equities and bonds does not guarantee a stable cash flow.

Traditional pension (defined benefit) plans have nearly disappeared:

Corporate defined benefit (DB) pension plans have largely become a thing of the past in the private sector. Annuities are now the only commercial product that can provide a "guaranteed lifetime income" stream.

Statement disclosure requirements are also changing:

Reform is pushing 401(k) account statements to display not just the "total account balance of $500,000," but also an estimate such as "this balance is equivalent to approximately $2,500 per month in retirement income." This small change will cause many people to reassess whether they've truly saved enough.

Is This Right for You? Consider Both Sides

Reasons to consider it:

• Establish a guaranteed income floor ahead of retirement—giving you peace of mind

• The rollover process generally does not trigger an immediate taxable event (when done as a direct rollover)

• Many modern annuities include long-term care (LTC) riders, so one product covers two types of protection

Questions to think through carefully:

• Liquidity will decrease: Once funds are moved into an annuity, there are typically surrender charge periods of 5 to 10 years—making it far less flexible than a 401(k) if you need cash in an emergency

• Fee structures require careful review: Some annuity products carry significant commissions and mortality & expense (M&E) charges that can erode returns over the long term

• Inflation is a hidden risk: Without an inflation protection rider (cost-of-living adjustment, or COLA), the purchasing power of the same monthly benefit amount will be significantly diminished 20 years down the road

What Should You Do Now?

The bill has already received a positive reception from the House Ways and Means Committee, and the market expects it may pass as part of a broader "Retirement 3.0" legislative package.

Before the bill is formally enacted, there are two things you can do now:

1. Check whether your existing 401(k) plan document already allows for "In-Service Withdrawal" provisions—some employer plans already permit this.

2. Consult a financial advisor to evaluate what percentage of your overall asset allocation should be allocated to annuitized income—this depends on your other income sources, health status, and household situation.

One Final Note

The U.S. retirement system is undergoing a quiet but profound shift: from an "accumulation culture" to a "distribution culture."

How much money is in your account is only the first step. The more important question is: can that money reliably show up in your bank account every single year that you need it?

That's a question worth thinking through well in advance.

Disclaimer: The content of this article is for informational purposes only and does not constitute financial or legal advice. Legislative content is subject to the final enacted text. Readers are advised to consult a licensed financial advisor for personalized planning.