2026 Retirement

2026 Retirement Planning: A Few Things You Need to Know

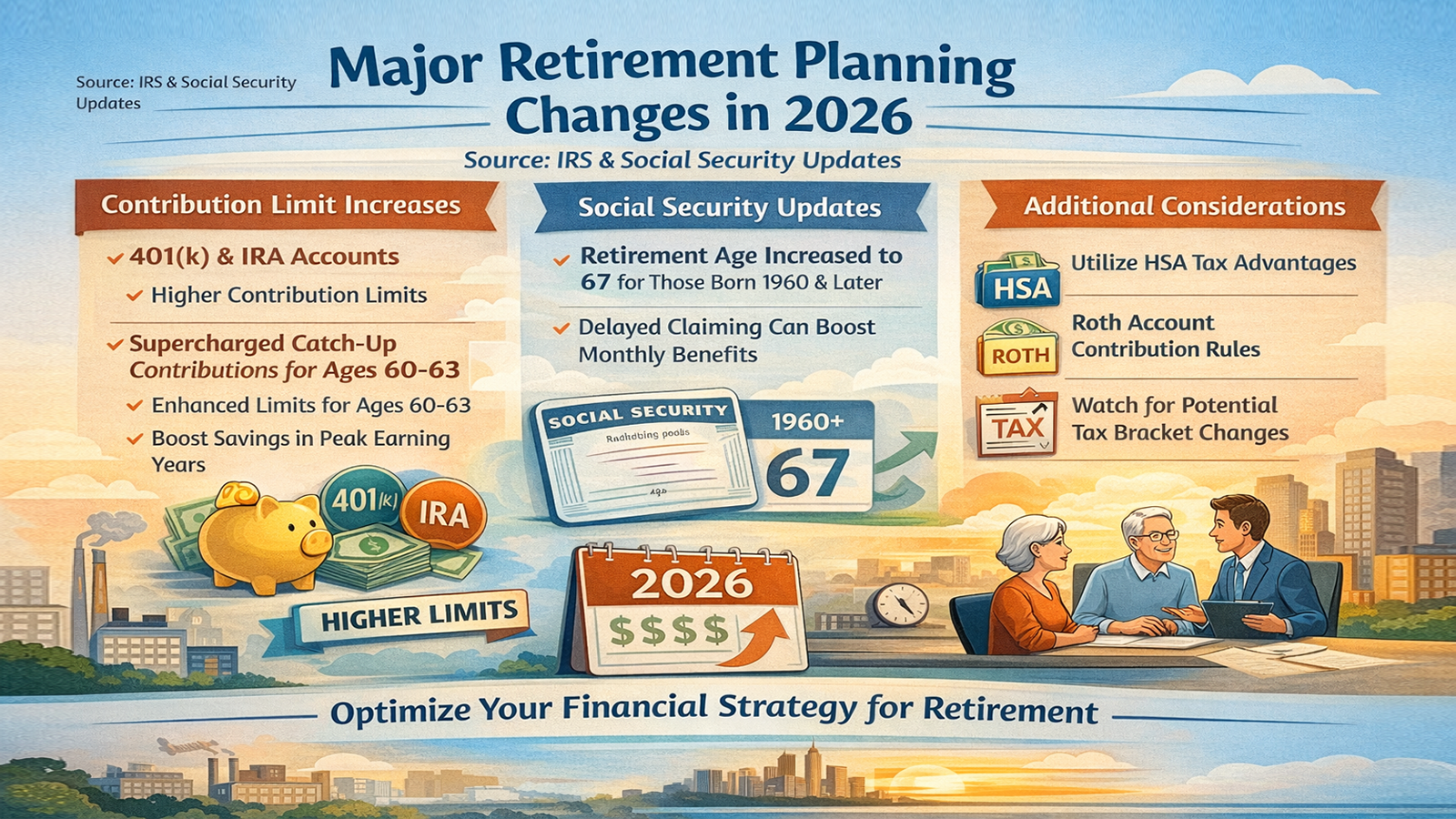

Retirement planning can sound like something far off in the future—but every year, when the IRS and the Social Security Administration (SSA) update their rules, how much you can save and how much you can collect both change along with them.

There are a few changes in 2026 that are especially worth paying attention to—particularly if you happen to fall in the 60–63 age range. There's a rare tax-advantaged opportunity this year that you really don't want to miss.

I. Retirement Accounts: How Much Can You Contribute This Year?

401(k) / 403(b) / 457(b) / TSP

The base contribution limit has increased: In 2026, each person can contribute up to $24,500, an increase of $1,000 from last year.

Age 50+ catch-up contributions: On top of the base limit, those aged 50 and older can make an additional catch-up contribution of $8,000, for a combined total of $32,500.

Special benefit for ages 60–63: This is the "super catch-up" provision introduced under the SECURE 2.0 Act. If you are exactly 60, 61, 62, or 63 years old this year, your catch-up contribution limit jumps to $11,250, bringing your total potential contribution to as high as $35,750. This window lasts only four years—if you're in this age range, it's genuinely worth taking full advantage of.

One note for high earners: If your prior-year income exceeded $145,000, your catch-up contributions must be directed into a Roth (after-tax) account—pre-tax catch-up contributions are no longer permitted above this threshold.

IRA / Roth IRA

The base contribution limit for 2026 has increased to $7,500. Those aged 50 and older can contribute an additional $1,000, for a combined total of $8,500.

If your income is on the higher side, be sure to check whether your Modified Adjusted Gross Income (MAGI) exceeds the Roth IRA income phase-out threshold. If it does, don't worry—you can still contribute via the Backdoor Roth IRA strategy. It's a good idea to confirm the exact steps with your CPA.

Don't Forget About Your HSA (Health Savings Account)

An HSA is the "invisible retirement account" that many people overlook—contributions go in tax-free, grow tax-free, and qualified medical withdrawals come out tax-free as well.

2026 contribution limits: $4,300 for individuals, $8,550 for families. It's worth maxing this out every year.

II. Social Security Benefits: When Is the Best Time to Claim?

Born in 1960 or Later? Your Full Retirement Age (FRA) Is Now 67

This is an important milestone in 2026: for everyone born in 1960 or later, the Full Retirement Age (FRA) is now officially set at age 67.

What does this mean in practice? Simply put:

• Claiming at 62 (early): You can—but your monthly benefit will be permanently reduced by approximately 30%.

• Claiming at 67 (FRA): You receive 100% of your standard benefit amount.

• Waiting until 70 (delayed): Your monthly benefit will be roughly 24% higher than at age 67. This is the maximum—waiting beyond 70 provides no further increase.

So the later you claim, the more you receive each month—but that assumes you're in good health and have a longer expected lifespan. It's worth running your numbers through the SSA's online calculator to find your "break-even point" and determine which strategy makes more sense for you.

2026 Benefit Estimates

• Claiming at 67 (FRA): Maximum benefit of approximately $4,118/month

• Delaying until 70: Maximum benefit approaching approximately $5,100/month

Of course, your actual benefit depends on your individual earnings history and lifetime contributions—everyone's amount will differ.

Cost-of-Living Adjustment (COLA)

Based on inflation projections, the Social Security Cost-of-Living Adjustment (COLA) for 2026 is estimated to be between 2.5% and 2.8%.

One thing to keep in mind: if Medicare Part B premiums increase at the same time, the net increase you actually see in your check may be slightly less than the COLA percentage.

Social Security Taxable Wage Base

In 2026, the Social Security taxable wage base—the maximum amount of earnings subject to the 6.2% Social Security payroll tax—is projected to increase to approximately $178,000. Income above this threshold is not subject to Social Security tax.

III. What Planning Actions Can You Take in 2026?

If you're between 60 and 63:

The super catch-up window is right in front of you. The extra $3,250 per year (compared to the standard age 50+ catch-up limit) is a legally granted opportunity to accelerate your retirement savings—don't let it go to waste.

If you're approaching Social Security claiming age:

It's worth recalculating whether delaying your claim still makes sense—your health, family circumstances, and other income sources all need to be factored in.

If you're a high earner:

Pay close attention to the Roth requirement for catch-up contributions this year. Also watch for the potential expiration of certain provisions under the Tax Cuts and Jobs Act (TCJA) at year-end—tax brackets may shift, and it's worth planning across tax years proactively.

Quick Reference Summary

Account Type |

2026 Contribution Limit |

Age 50+ Catch-Up |

Age 60–63 Super Catch-Up |

401(k), 403(b), 457, TSP |

$24,500 |

+$8,000 |

+$11,250 |

IRA / Roth IRA |

$7,500 |

+$1,000 |

— |

HSA (individual) |

$4,300 |

— |

— |

HSA (family) |

$8,550 |

— |

— |

Disclaimer: The content of this article is for informational purposes only. All figures are subject to final official publication by the IRS and SSA and do not constitute financial or tax advice. Readers are encouraged to consult a licensed financial advisor or CPA based on their individual circumstances.