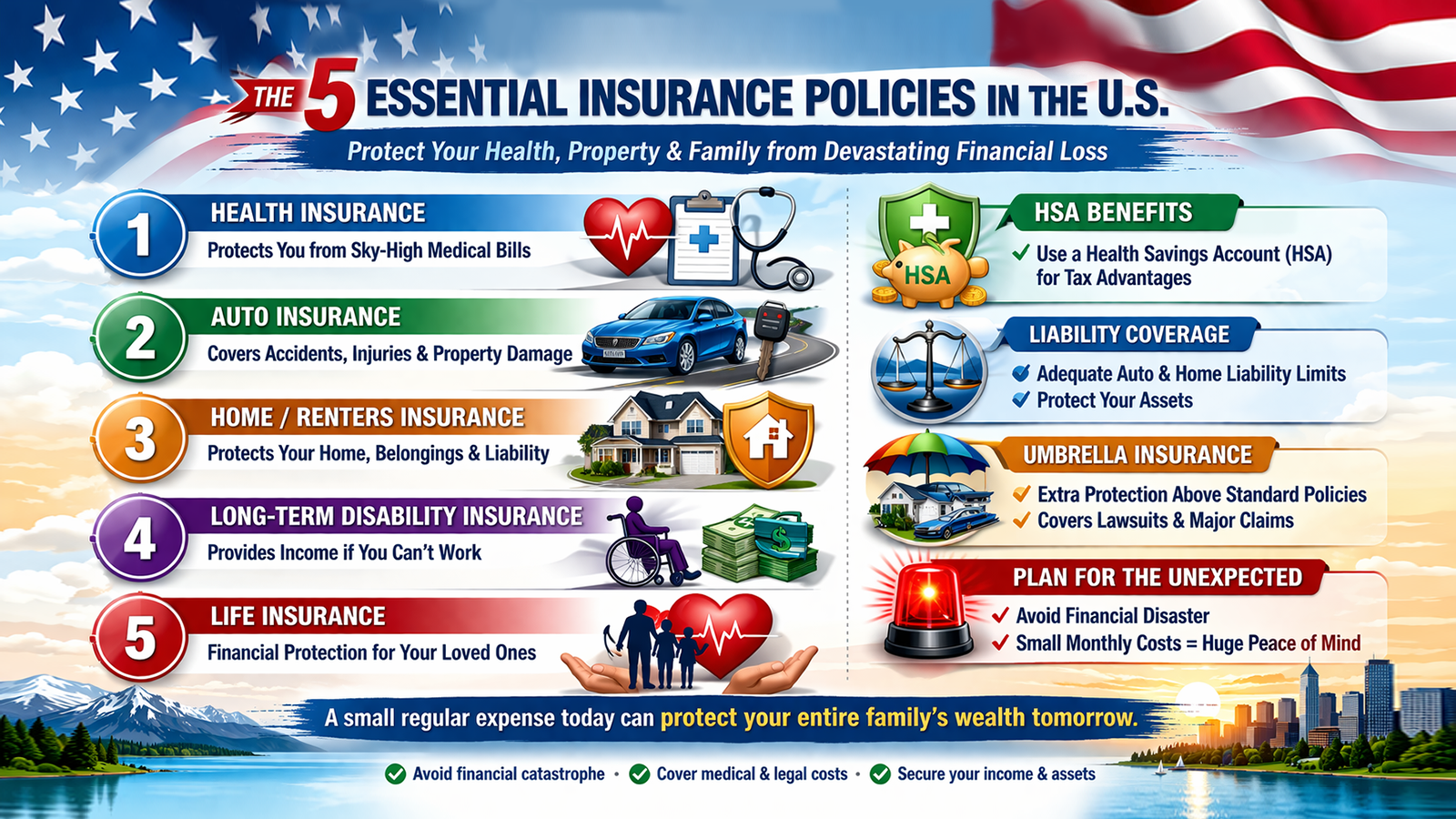

One Accident Away from Bankruptcy? The 5 Insurances That Protect You in America

Living in the U.S.? These 5 Types of Insurance Are Non-Negotiable

When it comes to insurance, most people's first reaction is: "Too expensive, too complicated, and I probably won't even need it."

But in the United States, the situation is completely different. Medical bills and litigation costs here can easily run into the hundreds of thousands of dollars. A single uninsured accident can wipe out years of a middle-class family's accumulated wealth in an instant. The logic behind insurance is simple—spend a little each month in exchange for the peace of mind that "the worst case won't be quite so bad."

Below, ranked by importance, are the five types of insurance most worth prioritizing.

#1 Health Insurance

Without health insurance, nothing else matters.

In the U.S., a single emergency room visit can easily cost several thousand dollars, and a hospital stay can run tens—or even hundreds—of thousands. Health insurance has the highest priority of all insurance types, bar none.

If your employer offers a group health plan, enroll in that first. If you don't have employer-sponsored coverage, you can purchase a plan through Healthcare.gov (the ACA Marketplace). Most people qualify for premium tax credits (subsidies), so the actual cost is usually lower than you'd expect.

A combination worth considering: If you're generally healthy, consider pairing a High-Deductible Health Plan (HDHP) with a Health Savings Account (HSA). Contributions to an HSA go in tax-free, grow tax-free, and qualified medical withdrawals come out tax-free—a true triple-tax-advantaged account designed specifically for healthcare expenses. Over the long run, it's an excellent deal.

⚠️ Short-term health plans are cheap, but they come with a lot of hidden pitfalls—they typically exclude pre-existing conditions and are restricted or unavailable in California and several other states. They should only be used as a temporary stopgap.

#2 Auto Insurance (Car Insurance)

The law requires you to have it—but the legal minimum is nowhere near enough.

Many states set the minimum liability coverage at just $25,000. But a serious car accident can generate medical bills that exceed that amount several times over.

Practical recommendation: Choose at least 100/300/100 liability limits—that's $100,000 per person bodily injury, $300,000 per accident bodily injury, and $100,000 property damage. If your household net worth is substantial, consider adding an Umbrella Insurance policy. For just a few hundred dollars a year, you can extend your total liability protection to $1 million or more—excellent value.

There's one add-on that a lot of people overlook: Uninsured/Underinsured Motorist (UM/UIM) coverage. If the at-fault driver flees the scene or doesn't carry adequate insurance, this coverage steps in to cover your medical expenses and vehicle damage. It happens more often in the U.S. than most people realize.

#3 Homeowner's Insurance / Renter's Insurance

Essential for homeowners, and strongly recommended for renters too.

If you own your home, make sure your policy is based on Replacement Cost coverage—not Actual Cash Value (ACV). ACV policies deduct depreciation from the payout, meaning the settlement may not come close to covering the cost of rebuilding your home.

If you're a renter, Renter's Insurance is remarkably affordable—sometimes under $20 a month—but provides genuinely useful protection: laptops, furniture, and clothing lost to theft or damage are covered. More importantly, it includes personal liability coverage—if you accidentally start a kitchen fire that spreads to your neighbor's unit, your policy handles the claim and the legal fallout.

⚠️ Whether you have homeowner's or renter's insurance, flood and earthquake damage are NOT covered under standard policies. If you live in a flood zone, purchase a separate policy through the National Flood Insurance Program (NFIP).

#4 Long-Term Disability Insurance (LTD)

Most people think life insurance is the most important coverage—but the reality is that "losing the ability to work" is far more common than premature death.

Picture this: an accident or serious illness suddenly leaves you unable to work—no income coming in, and possibly a need for ongoing care. That is the financial crisis that devastates many families.

Start by checking whether your employer offers Group Long-Term Disability (Group LTD) coverage. If they do, use it. If they don't—or if the benefit level isn't sufficient (group LTD typically replaces only 60% of salary and often has a benefit cap)—consider purchasing your own policy with an "Own-Occupation" definition of disability.

Why this definition matters: Under an Own-Occupation definition, as long as you're unable to continue performing the duties of your specific profession due to illness or injury, you're entitled to benefits—even if you could theoretically do some other type of work. For professionals such as physicians, attorneys, and engineers, this clause is especially critical.

#5 Life Insurance

If someone depends on your income, you need life insurance.

If you carry a mortgage, have children, or have a spouse who relies on your earnings—what happens to them if you're gone? Life insurance exists to answer that question.

Term Life Insurance is the best choice for most families: low premiums, high coverage amounts. A 20- or 30-year term policy can cover the life stage when you need protection most.

If your wealth has grown to a point where you need estate tax planning or wealth transfer strategies, Permanent Life Insurance may be worth considering.

Many life insurance policies today also include Living Benefits riders—if you're diagnosed with a critical illness such as cancer or a stroke while still alive, you can access a portion of the death benefit early to cover treatment costs. You don't have to wait until death to use the policy. This transforms life insurance from "protection after you're gone" into "protection throughout your life."

Quick Summary

Priority |

Insurance Type |

Why You Can't Skip It |

🥇 |

Health Insurance |

Medical costs in the U.S. are astronomical—going without is flying without a net |

🥈 |

Auto / Homeowner's Liability Insurance |

One accident or lawsuit can wipe out everything you've built |

🥉 |

Long-Term Disability Insurance |

Protects your most valuable asset—your earning capacity |

4️⃣ |

Term Life Insurance |

The baseline of financial responsibility to the people who depend on you |

Disclaimer: The content above is for informational purposes only and does not constitute legal or financial advice. Insurance policy terms vary by state. We recommend consulting a licensed insurance broker or financial advisor for guidance specific to your situation.