What Is Indexed Universal Life Insurance (IUL)?

What Is Indexed Universal Life Insurance (IUL)? Is It Worth Buying?

Many people hear the term "IUL" for the first time and their reaction is simple:

I have no idea what that means.

Insurance policy language is already complex enough, and with English abbreviations thrown in everywhere, it's easy to give up entirely. This article has one goal: to explain what IUL is, what it's good for, and what pitfalls to watch out for — in plain language you can actually understand.

This article is for informational purposes only and does not constitute financial or legal advice. IUL products have complex structures. It is recommended that you consult a licensed broker based on your personal situation.

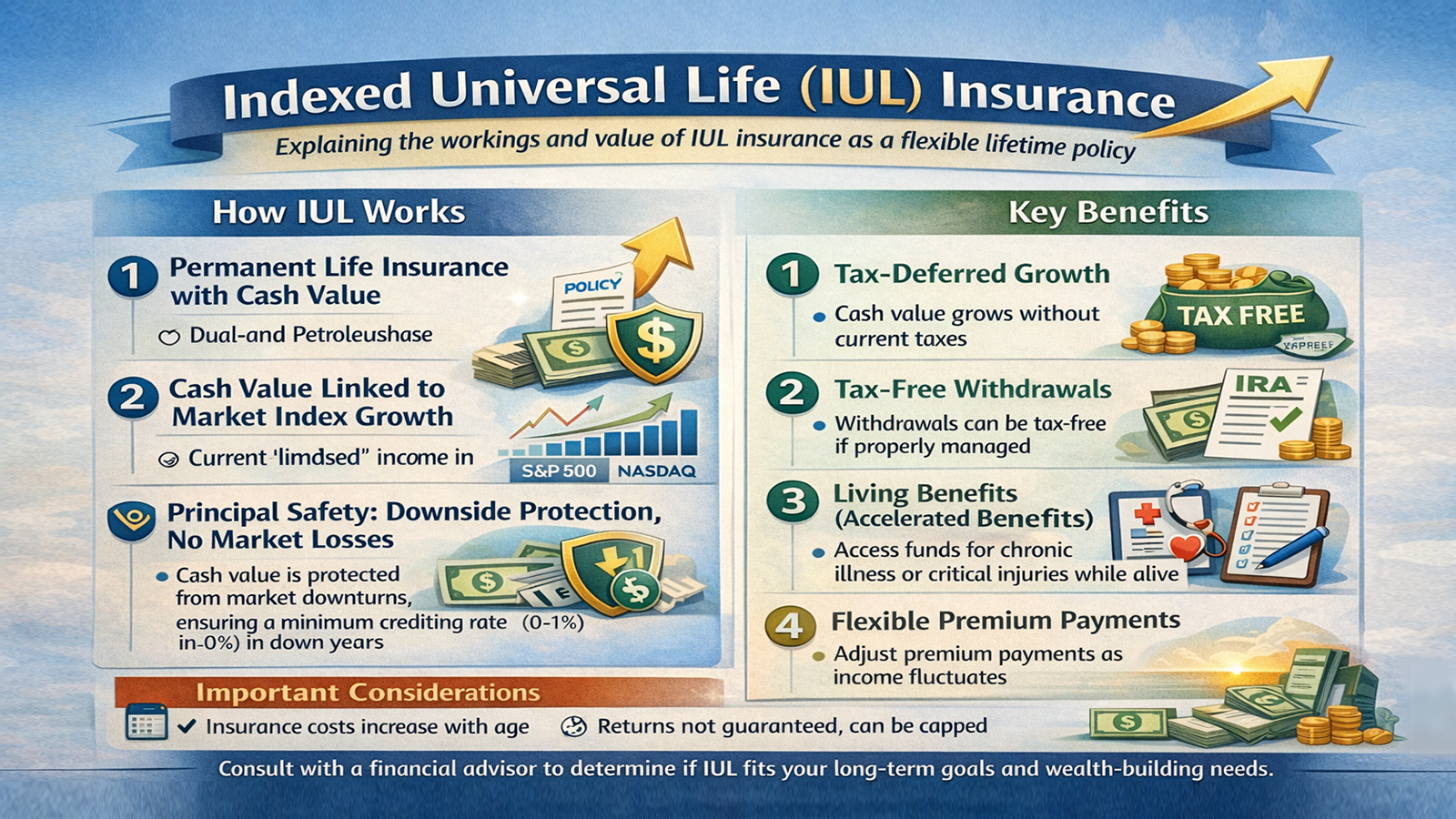

The Basics: What Is IUL?

IUL stands for Indexed Universal Life. It is a type of permanent life insurance, meaning that as long as you continue paying premiums, coverage stays in force for life — unlike term life insurance, which expires at the end of the policy term.

The biggest difference from ordinary life insurance is that the money inside the policy can "grow."

Each month, a portion of your premium covers the cost of insurance; the remainder goes into a "cash value account." The way this cash value grows is somewhat unique:

• When markets go up: The account is credited based on a market index — such as the S&P 500. When the index rises, your account earns interest at an agreed-upon rate.

• When markets go down: The account has a "floor rate," typically 0%, meaning even if the market crashes, the principal in your account will not lose value.

In short: gains are tied to the market; losses are protected by a floor.

What's New in 2026?

① You Can Now Contribute More

The U.S. tax code (Section 7702) was revised in recent years, allowing policyholders to put more money into a policy for the same death benefit without triggering "MEC" status (once a policy becomes a Modified Endowment Contract, its tax advantages disappear). Simply put: IUL now has more room to store cash than before.

② Cap Rates Are Moving Targets

Your earnings have a ceiling — called the "Cap Rate." Even if the market climbs 30%, you only receive up to the cap, which is typically 8%–12%. This number is not fixed; insurance companies adjust it periodically based on market interest rates. Ask about it before you buy.

③ Read Multiplier and Bonus Clauses Carefully

Some products promise a "multiplier effect" that amplifies your returns. This sounds appealing, but there's no free lunch — these products typically carry higher fees, and the real benefit only shows up after years of holding. Don't be dazzled by illustration numbers.

What Are the Practical Benefits of IUL?

The "Triple Tax Advantage"

This is the core reason many people choose IUL:

• Tax-deferred growth: Money compounds inside the policy without requiring annual capital gains tax reporting.

• Tax-free withdrawals: When structured correctly, accessing funds through "policy loans" does not count as taxable income in the year taken.

• Tax-free death benefit: When you pass away, the insurance proceeds go directly to your beneficiaries, generally free of federal income tax.

For high-income individuals, these three benefits combined make IUL a genuinely attractive tax-planning tool.

"Living Benefits" — Insurance You Can Use While Alive

Modern IUL is not just useful after you die. If you are diagnosed with cancer, require long-term care, or develop another serious illness while still living, you can access a portion of the death benefit early to cover treatment and living expenses. This transforms IUL from "protection after death" into "protection for life."

Flexible Premium Payments

Unlike traditional whole life insurance, IUL does not require you to pay the same fixed amount every month. In a good income year, you can contribute more; when money is tight, you can pay less or even pause — as long as the cash value in your account is sufficient to cover the cost of insurance, the policy will not lapse.

A Buffer Against Market Volatility

For those who "don't want to go all-in on the stock market, but think bank interest rates are too low," IUL offers a middle ground: upside potential with downside protection.

Pitfalls You Must Know Before Buying

IUL is genuinely powerful — but if you don't understand the following, you may run into serious problems.

Pitfall #1: Insurance Costs Rise with Age

The Cost of Insurance deducted each year increases as you age. If the cash value in your account cannot grow fast enough to keep pace with rising costs — and you don't top up your premiums — the policy may eventually lapse, and all the premiums you paid could be lost.

Pitfall #2: Illustrated Returns ≠ Guaranteed Returns

The illustrations brokers show you typically assume an annualized return of 6%–7%. This is an assumption, not a promise. If markets stagnate for an extended period, actual results could fall far short of expectations. When you receive an illustration, always ask to see a projection under a "low-return scenario" as well.

Pitfall #3: Early Surrender Comes at a High Cost

IUL typically carries a surrender charge period of 10 to 15 years. If you decide to withdraw all your money only a few years after purchasing, you will face substantial penalties. This is not a product designed for short-term use. Before buying, ask yourself honestly: can I leave this money untouched for the long term?

Who Is IUL Best Suited For?

High-income earners: Those who have already maxed out their 401(k) and IRA contributions and are looking for additional legal tax-advantaged savings vehicles.

Middle-aged families: Those who need substantial coverage for their families while also wanting to build a supplemental fund over 15–20 years for their children's education or their own retirement.

Foreign nationals holding U.S. assets: IUL can be an effective tool for allocating USD-denominated assets and reducing estate tax exposure, though specific eligibility requirements apply. Professional consultation is recommended.

A Final Word

IUL is a powerful financial instrument — but it's more like a precision machine that requires careful calibration and long-term maintenance. Designed well, it can help you achieve tax efficiency, asset protection, and retirement planning. Designed poorly — or purchased as a product that doesn't fit your situation — it can cause real harm.

Before you decide, the two most important questions to ask yourself are:

Am I buying this primarily for supplemental retirement income? Or to leave a substantial death benefit and living benefits for my family?

Get clear on your goals first, then work with a qualified, licensed broker to structure the policy to your specific needs — that is the right way to approach IUL.