Is Social Security Running Out? The Truth Is More Complicated Than You Think

Is Social Security Going Bankrupt? The Truth Is More Complicated Than You Think

You may have heard this before: "Social Security is running out — by the time we retire, there might be nothing left."

That statement is half right — and half wrong. Social Security will not disappear, but if Congress does not act, the checks you receive in retirement could be about 20% smaller than you expect. These are two very different things, and it is worth understanding the distinction.

Let's Start with the Facts: What Is Actually Happening?

Simply put, Social Security works like this: people working today pay taxes that fund today's retirees.

The problem is that Baby Boomers (born 1946–1964) are retiring en masse, while declining birth rates mean there are fewer workers entering the workforce behind them. Less money is coming in; more money is going out — and the trust fund reserves are slowly being drawn down.

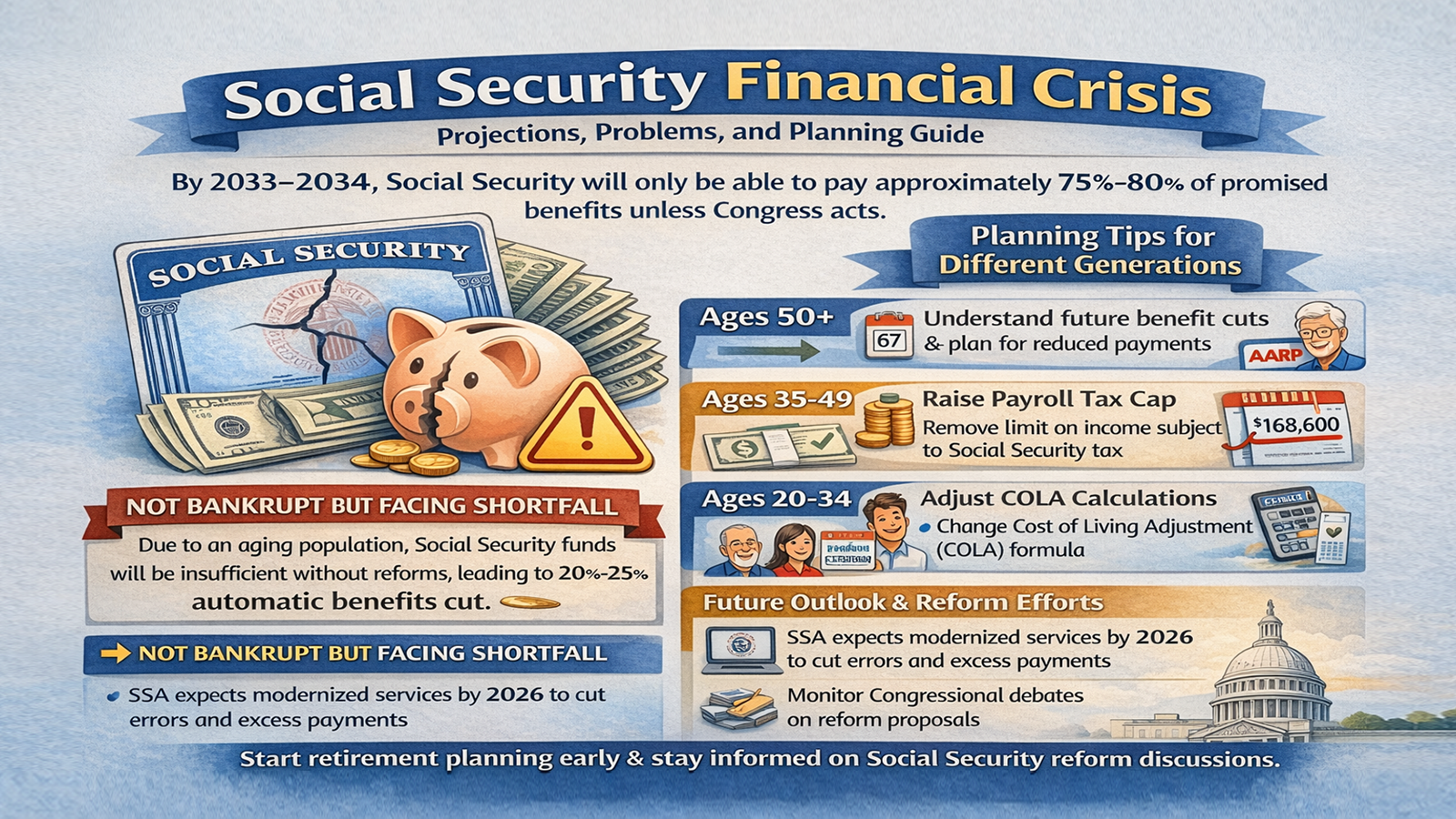

According to the SSA's latest actuarial report, if nothing changes:

• Around 2033–2034, the OASI (Old-Age and Survivors Insurance) trust fund reserves will be depleted.

• At that point, the SSA would only be able to pay benefits using the payroll taxes collected in that same year.

• This means every retiree's check could automatically be reduced by roughly 20% to 25%.

To be clear: this is not zero — it is a reduction. As long as people are working and paying taxes, Social Security will continue to exist.

How Might Congress Fix This?

This is the heart of the 2026 policy debate, and three main approaches are on the table. The impact varies considerably depending on your age.

Option 1: Raise the Full Retirement Age Further

The current Full Retirement Age (FRA) is already 67. Some proposals would push it to 69 or even 70. The impact on people already retired or close to retirement would be minimal — but if you are in your early 40s today, you may need to work two or three years longer than your parents did to receive full benefits. This is one of the most subtle forms of a "stealth benefit cut."

Option 2: Require Higher Earners to Pay More

Currently, income above approximately $178,000 is not subject to Social Security payroll tax. Reform proposals are considering eliminating this cap entirely, or reinstating the tax on earnings above $400,000. This would inject more funding into the system, though the retirement benefits for high earners would not increase proportionally — effectively asking higher-income individuals to shoulder a greater share of the system's costs.

Option 3: Adjust How COLA Is Calculated

COLA (Cost-of-Living Adjustment) is the annual inflation-based increase applied to Social Security benefits. Some proposals suggest switching to an index that better reflects seniors' actual spending patterns — especially healthcare costs — known as the CPI-E. This could result in slightly higher annual increases. However, it is a double-edged sword: higher payouts drain the trust fund faster, so this option would typically need to be paired with a tax increase to be viable.

How Should You Think About This at Different Life Stages?

Already Retired or Close to Retirement (Age 62+)

Near-term risk is relatively low. Politically, cutting benefits for people already receiving them faces enormous resistance — there is virtually no historical precedent for it. The bigger thing to watch is: rising Medicare premiums that quietly erode your net Social Security income. This impact is often overlooked.

Middle-Aged (Ages 45–60)

This group has the most need to plan proactively. The FRA may be pushed back; higher earners may face increased tax burdens. Now is a good time to accelerate 401(k) and IRA catch-up contributions — with the goal of reducing your dependence on Social Security rather than counting on it to arrive in full and on time.

Younger Generation (Under 45)

The rules will almost certainly change — we just do not know exactly how. The most prudent mindset is: treat Social Security as a bonus, not the foundation of your retirement plan. Your personal savings and investments are the pieces you can actually control.

A New Development in 2026: Reducing Improper Payments

Beyond the broader reform debate, the SSA is also strengthening its internal operations: real-time cross-referencing against the national death records database to prevent fraudulent claims, along with a major push toward digital processing. Starting in 2026, the vast majority of new applications will be handled through an upgraded "My Social Security" online account, reducing manual errors. These measures will not solve the underlying financial shortfall on their own, but they do improve how efficiently existing funds are used.

Final Thoughts

Social Security was never designed to fund a "comfortable retirement" on its own — it was always meant to be a safety net, not a full income replacement.

A solid retirement plan typically rests on four pillars:

Government benefits (Social Security) + Employer plans (401k/403b) + Personal investments (IRA/real estate) + Private insurance (annuities/IUL/long-term care)

2033 is still nearly a decade away — there is still time. What matters is starting to plan now, rather than waiting until the rules actually change before reacting.

Disclaimer: This article is for informational purposes only and does not constitute financial or tax advice. Specific data should be verified against official publications from the SSA and IRS. Please consult a licensed financial advisor for personalized planning.