Hidden Retirement Taxes

Moving to a No-Income-Tax State Will Save You Money in Retirement — Right? Not So Fast.

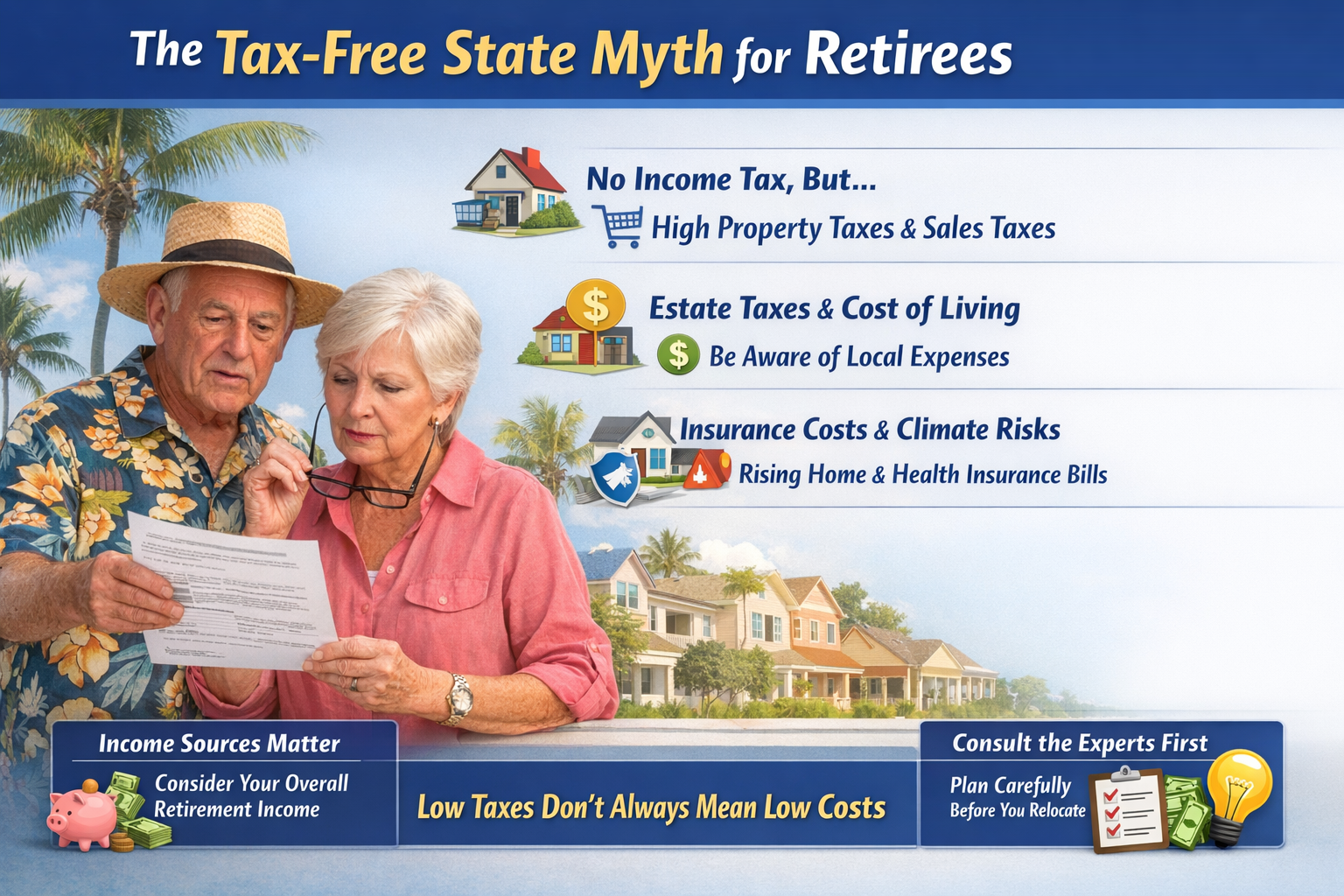

When many people start planning for retirement, their first instinct is: "Move to Florida or Texas — no state income tax, big savings!"

That instinct is not wrong, but it is only half the story. Tax revenue is essentially conserved — if the state does not collect it on income, it will find it through property taxes, consumption taxes, or estate taxes. Focus only on income tax while ignoring other hidden tax burdens, and you may find yourself sorely disappointed after the move.

Which States Actually Have No Income Tax?

As of 2026, there are 9 states in the U.S. that do not levy a personal income tax:

Florida, Texas, Tennessee, South Dakota, Nevada, Washington, Wyoming, Alaska, and New Hampshire.

New Hampshire is the newest addition — it fully eliminated its tax on interest and dividend income in 2025, officially joining the zero-income-tax camp. That sounds great. But the four categories of taxes below are the ones you really need to work through carefully.

Hidden Tax #1: Property Tax — The "Invisible Mortgage" of Retirement

In states without income tax, local governments typically rely on property taxes to fund schools and public services — which means property tax rates tend to run high.

• Texas: Zero state income tax, but effective property tax rates have consistently ranked among the highest in the nation.

• New Hampshire: One of the heaviest property tax burdens in the entire country.

There is also an important issue to watch specifically in 2026: home values across the country have surged over the past several years, and even if the tax rate stays the same, a higher assessed value means a bigger tax bill. For retirees on a fixed income, the scenario of "living in a million-dollar home but struggling to pay the property tax bill" is no joke.

Hidden Tax #2: Sales Tax — A Quiet Cut From Every Purchase

Sales tax has a key characteristic: the lower your income, the heavier the burden. Because lower-income households spend a larger share of their income on consumption, the same tax rate hits retirees proportionally harder than it did during their working years.

• Washington State and Tennessee: Combined sales tax rates (state + local) typically run around 9% to 10%.

In retirement, the bulk of everyday spending goes toward daily necessities, dining, and leisure — and nearly every dollar spent carries an extra 9–10% tax charge. Over time, that adds up to a meaningful sum.

Hidden Tax #3: State Estate Tax — A Lifetime of Saving, Still Taxed at the End

The federal estate tax exemption is very high, and most people will never come close to it. But some states impose their own estate taxes, with much lower thresholds.

Washington State is a prime example — no income tax, but it has its own state-level estate tax with an exemption of only around $2 million.

A real-world scenario: a retiree who spent many years in Seattle saved a considerable amount by paying no state income tax — but upon passing away, the combined value of the home and remaining 401(k) balance could easily trigger the state estate tax, significantly reducing what gets passed on to the children. Saving on income tax and leaving a healthy inheritance are sometimes two separate things.

Hidden Tax #4: Inheritance Tax — Not Your Bill, Your Children's

This tax is even easier to overlook. Inheritance tax is not paid by the deceased — it is paid by the people who inherit the assets. Currently, only 6 states impose it: Pennsylvania, New Jersey, Maryland, Kentucky, Nebraska, and Iowa.

Think this does not apply to you? Not necessarily. If your children live in one of these states, or if some of your assets are located there, the tax chain can become surprisingly complicated. This is a blind spot many people do not anticipate when doing estate planning.

Beyond Taxes: Three More Costs to Factor In

Healthcare costs: Medicare Advantage plan premiums and long-term care insurance (LTC) rates vary significantly from state to state — these numbers cannot be ignored.

Cost of living: Texas and Florida summers are brutally hot, and high air-conditioning bills can quickly eat up whatever you saved on taxes.

Homeowner's insurance: In coastal areas of Florida and Texas, hurricane and climate risk has pushed home insurance premiums to thousands — or even tens of thousands — of dollars per year in recent years. This is a number you must calculate carefully before deciding to move.

How Do You Decide Whether Moving Is Actually Worth It?

The core question is: where does your retirement income come from?

If your income is primarily from Social Security and a Roth IRA, both of which already carry very low tax burdens, the marginal benefit of moving to a no-income-tax state is actually quite small — and it may well be offset by higher property taxes.

If your income is primarily from a traditional 401(k)/IRA or large taxable investment accounts, you are facing meaningful annual federal and state income tax bills — and that is when relocation can genuinely deliver significant tax savings.

One Final Thought

The lowest-tax state is not necessarily the right state for you.

Choosing where to retire should be a balanced decision weighing taxes, healthcare access, climate, and your social network — not just a comparison of income tax rates on a single chart.

Before making a decision, it is well worth consulting a financial advisor who is familiar with multi-state tax issues and running the numbers for your specific situation. That consultation fee is almost always cheaper than discovering after the move that you did the math wrong.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Tax laws vary by state and are subject to change. Please consult a licensed tax or financial professional for a personalized assessment.